Good morning.. Asian stocks (those open) moved higher after a better close on Wall St which was boosted by the US Treasury announcement that they will be borrowing $3trln in Q2 to pay for virus relief. That’s a lot of issuance coming through the illiquid summer months but I guess the Fed will pick up the lions share. Stocks also got a boost as the NY Fed announced to the world that it would start buying those ETFs in early May. Why would they do that when they must know the front-running would be free money; isn’t that encouraging and illegal move? I do not understand how or why they would do that as it is encouraging front-running. Moving on, equities are firmer this morning and the USD weaker but EUR is still struggling and rightly so with all it faces this week. Today, the German Constitutional Court Hearing at 09.00bst on whether ECB’s PSPP program is legal under German law and tomorrow it will be seen if the EU can agree on a 7yr budget (expect a delay) and how to deliver the rescue package. I am not sure they can agree. Also I am getting rather concerned about the US administrations increased bad rhetoric over China; the markets are in no shape to see the trade war back on the radar but I think it is about to show up. Also what’s the tipping point for when bankruptcies become systemic? ISM non-manufacturing from the US the main data today.

Keep the Faith..

Details 05/05/20

FX traders waking up to what faces the EU this week.

–

It was a relatively quiet session yesterday but of note was some EUR weakness which to be honest was of little surprise to me with all that the EU is facing this week and I covered a lot of this yesterday. EUR dipped below 1.0900 and I think we may see more weakness as the week progresses as it seems there may be a delay coming and that is not what investors want to see. The lack of urgency within the EU on this delivery of the recue package says it all really and sums up this bureaucratic bunch. An Italian paper suggested that the focus of the Eurozone focuses on the fate of the Recovery Fund, which the Eurozone is expected to discuss on May 6th. But the premises are not good neither on the times nor on the contents. Vera Jourova, vice-president of the Commission, said that the proposal for the Recovery Fund will shift to the “second or third week of May” and the operation of the fund for January 2021 is an “ambitious” objective. Can kicking again and I just wonder is there is anything that can bridge this gap between Italy, Spain and France and Germany and the Netherlands. EUR is also starting to erase some of the technical support seen last week.

This a 4hour chart of EUR. EURJPY also moved lower through the session and I think this also could continue. German Constitutional Court Hearing today at 09.00bst on whether ECB’s PSPP program is legal under German law.

But stocks were higher in Asia overnight and I think generated by two specifics. The rally in Wall St into the close was based on a stunning announcement from the US Treasury which flowed into Asia markets (those that were open). Mnuchin announced that the Treasury was to borrow a record $3 trillion in the second quarter to pay for the coronavirus relief measures passed by Congress. Looking ahead to the third quarter, Treasury said it expects to borrow $677 billion. This of course means we are going to see some massive issuance coming through the quieter summer months but markets focuses on the stimulus again. It is clear that dwindling tax receipts are causing a balance of payments problem at the Treasury. In addition to this it was reported that scientists had created an anti-body in the lab that can defeat the virus and I think this also gave stocks a boost, along with rising oil prices overnight. In addition it was announced by the NY Fed that the Fed would probably start buying those ETFs early in May and this is a clear encouragement to front-run the Fed (illegal surely). Why would they announce that? This has seen the USD dip and a small recovery in some of the commodity currencies; but EUR remains stuck at 1.0900 and the EUR crosses all lower.

4hour chart EURJPY.

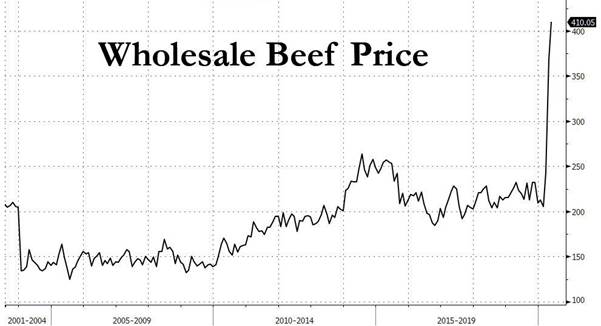

Meanwhile job losses keep coming as GE cuts 10k from its workforce as the aviation industry implodes. United air is to cut 30% of managers and admin staff and Mnuchin warned that air travel in the US may not restart any time soon. In the UK nearly 6m have applied for furloughed benefits and Friday’s NFP data could be a real stinker. It is suggested that Hertz is about to file for bankruptcy as the start of the corporate defaults picks up pace. Volkswagen says the cost of crucial car components has risen sharply because of the coronavirus outbreak, putting further pressure on profits as the industry enters deep recession. Are prices about to explode higher in an attempt to make up for lost earnings or is demand so bad that this practice will not help? Who picks up the tab for rising prices? Meat prices in the US are surging higher and many businesses are facing collapsing margins and thus earnings.

It is certainly something to watch for and going forwards and I would keep an eye on PPI data for signs of steep rises at the factory gates. But consumers will balk at higher prices in a slowdown or recession.

I am not sure at all that I fancy stepping onto a plane, or a train for that matter; but many will be forced back onto public transport if businesses reopen; can you keep your distance on a tube or train? Remember when thinking about that, that there is still no vaccine in sight. The danger of a relapse in the numbers seems large to me. Unions are starting to get involved about the safety of their workers and some workers may prefer to stay away and work from home if at all possible. But the economies around the globe need to restart and so the gamble (a political one) seems to justify unlocking. I hope they get this right but can many businesses go back to normal as working from home, home delivery and the general use of the internet has moved us all on exponentially; we have catapulted into the future. This will have a profound impact on many established industries in my view. The business world has in fact, already changed in a startingly short period of time.

Just as an example, Mall operators and department store owners have seen a preview of what their future was already going to look like. Many small restaurants and corner stores will never reopen because “cloud kitchens” or the 24-hour pharmacy will have taken their places. Gym operators may find that clients accustomed to exercising at home may not attend as frequently. Many have discovered a new way of doing things and a new way of life for some. Values are changing and in some cases for the better; but the point is things HAVE changed. Why travel if you don’t have to and business meetings using facetime, Zoom or video calls are now part of everyday business life and about time too; we have finally embraced the technology on offer. Unfortunately, the downside of this is the casualties and it is here where the problem lies as many may default and choose bankruptcy putting a huge strain on the lenders and bond holders and in some cases after years of simply massive equity buybacks which benefitted the management. Are we about to see a dangerous glut of empty office space where supply massively outstrips demand and commercial prices collapse?

But yet again I am drawn back to the consumer and the damage this has done to their mindset in all this. Headlines of huge job losses is not about to see a return to non-essential shopping and the danger here is that this fear of losing ones job, or the thought of surviving a deep recession, will impact spending decisions. Consumers rarely (never) see a V-Shaped recovery after a massive increase in unemployment or while facing an imminent recession. Therefore earnings for many businesses are in danger of literally collapsing in some cases. This virus has been a wake-up call in so many ways and our attention has shifted from celebrity and wealth to the importance of those who nurtured us through all this and it has brought issues like climate change back onto the agenda. Governments may have to start listening to that in some countries. Again, attitudes are shifting quickly and governments had better start listening as we are in the mood for change. Maybe this virus has been a defining moment for mankind; its about time we woke up from our slumber. We have been fed “bread and circuses” for too long. Talking of empires (Rome used the “bread and circuses” analogy), the US is making the same mistakes now that the UK made in the 1920s by moving deeper and deeper into debt. Nobody seems to learn the lessons of history; one day it will matter.

Equity markets in the US, after a 35% rally from the lows, appear to be taking a breather and may start to take a look at support down near 2650 on the broader macro weekly charts (the 200-week moving average). We may now be in a range but for me the charts seem to be rolling over again. Meanwhile, the 50-week moving average (currently 2992) provides resistance.

Certainly the fundamentals, in my view, are screaming that investors have not priced a U-shaped (or worse) recovery or the damage done to the consumer or the potential rise in defaults. The idea of a rapid bounce back to where we were seems nuts to me. Maybe some of this euphoria needs to cleanse itself but US stocks rallied into the close again last night in the absence of any more China bashing from Trump and the huge borrowing from the Treasury. But Trump is electioneering now and needs scapegoats and bad guys to blame everything on and in Navarro he has a willing vehicle to prod the Tiger. The trade war has not gone away and it seems the US administration want some kind of reparation from China; good luck with that chaps.

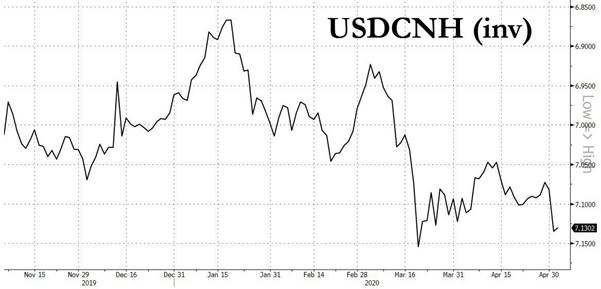

This was never about trade; this was always about positions on the global stage; hegemony and this is not going away as long as Trump is in office and the more he prods the Tiger the weaker the CNH will get. There is a very real risk now that relations between these two superpowers dissolve.

Chinese state media unleashed a torrent of criticism against Secretary of State Michael Pompeo — calling him “evil” and a liar — as Beijing sought to push back against the U.S.’s virus allegations without prompting a confrontation with President Donald Trump. That’s going well then! Keep an eye on this USDCNH move, as we are close to some very important levels here (key thresholds to watch are 7.1545, which was the high seen this year so far, and then 7.1940, which was the high seen before the “phase one trade deal” was signed). Trump stated that if China does not purchase US goods in line with the “phase one trade deal” that he will terminate it. This is so far, seen as Trump grumbling but with this guy he could react and say too much or cancel a deal if it does not suit him and China may be prepared to play the long game and try and play him out of his term. Xi has all the time in the world while Trump needs to win an election in November but how far will he go with China as stocks are in no shape to deal with an escalation in the trade war now; they would dump and I am sure he knows it.

There appears to be quite a bit of social unrest across America on the lockdowns and this could boil over and impact Trump’s chances of getting re-elected and so he needs a diversion and that may see the administration get tougher with China. This is a massive gamble with things as they are. Trump realises that the economy could be in tatters into the election and he needs to deflect from that. I am quite concerned by the increased rhetoric with China. The morale of US citizens is low and this Friday’s NFPs may make depressing reading and we need to monitor the earnings data too. Trump has seen his popularity scores rise while bashing China in the past and will likely go again if pushed. This, if it indeed escalates, is bad for everyone but Asia will feel it most but also those closely associated with China growth like Oz and the EU. I think the battle lines are being drawn up again as Trump looks for votes. That is not good for equities, which are especially sensitive right now or for the global economy; his gamble could very well backfire; big time.

—————————————————————————————————————-

Strategy:

Macro:.

Long USDCAD 1.4140. Stop 1.3850ish.

Short AUDJPY @ 69.25 added at 68.25 and Stop at 70.25 recent high.

Brought to you by Maurice Pomery, Strategic Alpha Limited.

—————————————————————————————————————-

Strategic Alpha Report Disclaimer

Doo Prime endeavor to ensure the reality, adequacy, reliability and accuracy of all the information provided, but do not guarantee its accuracy and reliability. All the information, analyses, comments, statements, and/or data provided in this report is for information purposes only. Client’s use of any contents of the report as the basis for the transaction, the client shall fully aware of the risks and agreed to bear all the risks. Client shall cautiously judge the accuracy of the information. Doo Prime has no liability for any loss caused by any inaccuracy or omissions of the contents and subjective reasons of Client.