May 2026 Non-Farm Payrolls Beats Expectations, But Markets Sell Off

The May 2026 Non-Farm Payrolls report beat expectations sharply, but the details suggest the US labor market may not be strong enough to justify a Fed rate hike.

At first glance, the number looked hot.

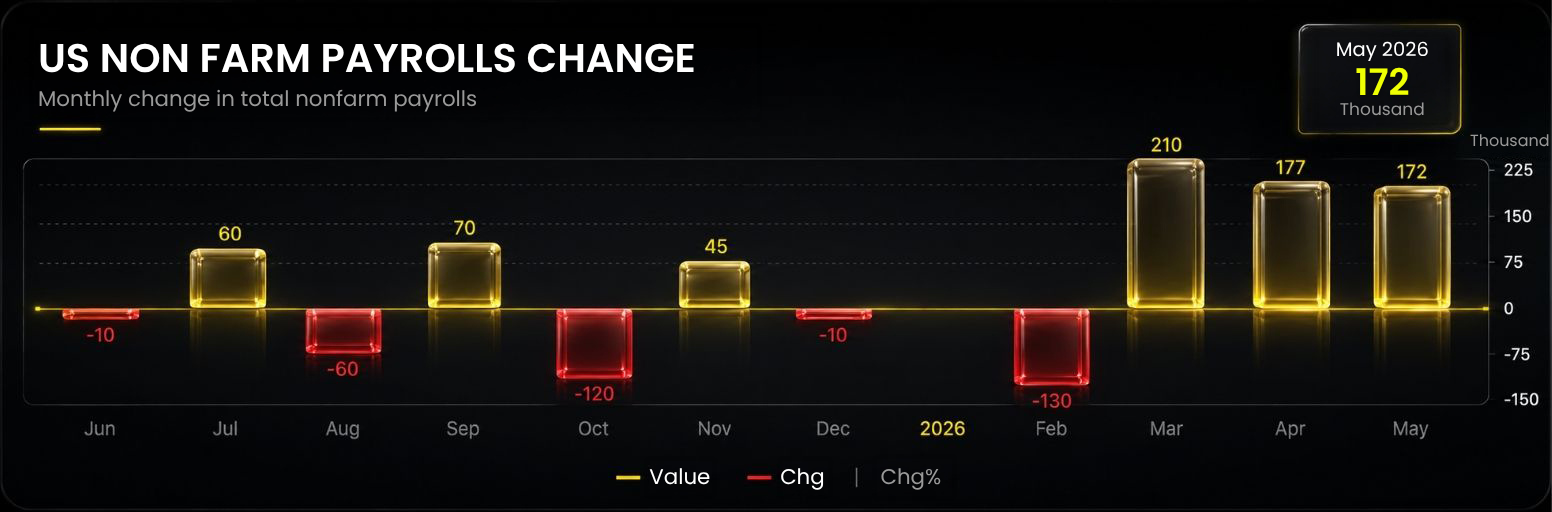

The US economy added 172,000 jobs in May, far above the market consensus of 85,000 and significantly higher than April’s 115,000.

Image Source: Trading Economics

Markets reacted fast.

Gold and stock indexes saw a broad sell-off. Gold fell 3.3%, S&P 500 futures dropped 2.9%, and the US Dollar Index rallied sharply.

At first glance, that reaction may look strange.

If employment is strong and the economy still looks resilient, why did stocks fall?

The answer is liquidity.

A strong economy, combined with elevated oil prices, makes it harder for the Fed to justify rate cuts this year. No rate cuts means no fresh liquidity. And without fresh liquidity, risk assets can struggle to find new buyers.

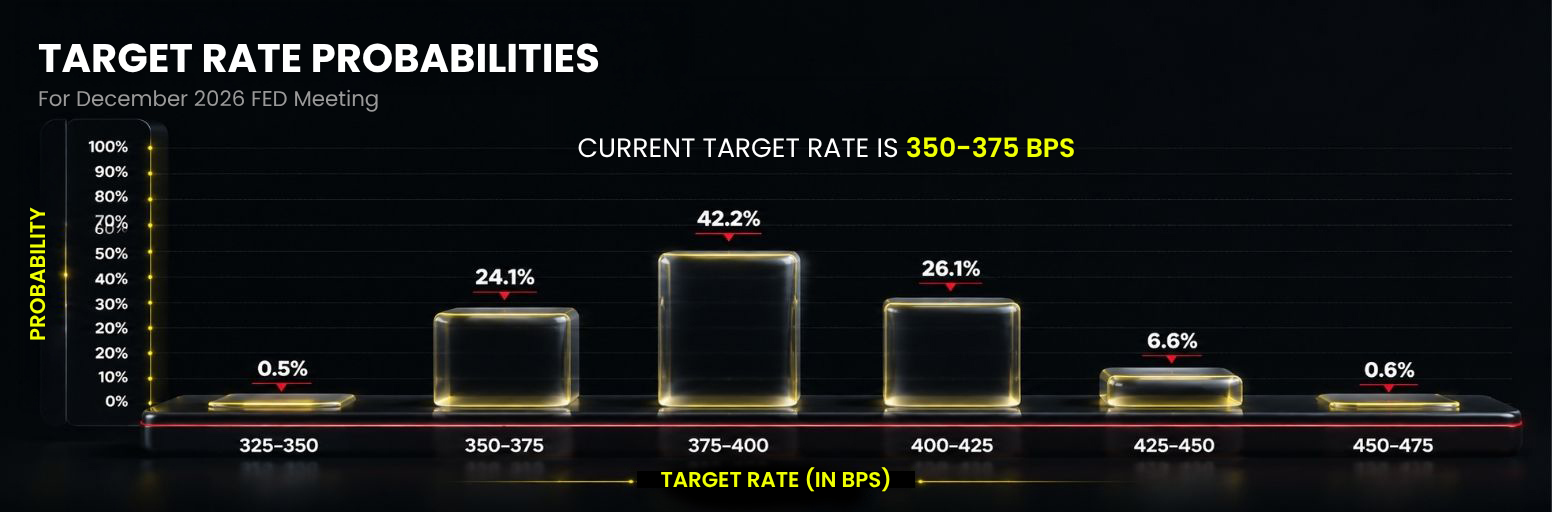

The market is now even pricing in the possibility of another rate hike.

According to CME data, the probability of a Fed rate hike by December has climbed to 75.5%. The most likely scenario is a single 25-basis-point hike, with a probability of 42.2%.

However, D Prime notes that market reactions may appear to be somewhat of an overreaction.

Could the Fed raise rates in 2026?

Yes, it is possible. But the odds may not be as high as the market currently thinks.

The World Cup May Be Distorting the Jobs Beat

The first thing traders should look at is where the job gains came from.

May’s employment growth was mainly driven by:

- Construction: 17,000 jobs

- Government: 52,000 jobs

- Healthcare: 35,200 jobs

- Leisure and hospitality: 70,000 jobs

The biggest surprise came from leisure and hospitality.

Compared with April, the hospitality sector suddenly became the main driver of job growth. Out of the 172,000 total non-farm jobs added in May, 70,000 came from hospitality alone.

Why?

Do not forget the biggest sports event of 2026: the FIFA World Cup.

The 2026 World Cup is co-hosted by the United States, Canada and Mexico. It is the first World Cup in history hosted by three countries, and the first expanded “Super World Cup” with 48 participating teams.

The tournament runs from June 11 to July 19, 2026. Out of the 16 host cities, 11 are in the United States.

That means hotels, restaurants, tourism operators, transportation services and event-related businesses may have increased hiring ahead of the tournament.

The high job gains in the government sector may also be linked to World Cup-related demand, including security and public service staffing.

This type of hiring is likely temporary. Once the tournament ends, the employment boost may fade.

In other words, the headline jobs number looks strong, but the underlying momentum in private-sector employment may be much more moderate.

Part-Time Hiring May Be Holding Up Employment

The broader labor market also does not look as hot as the headline number suggests.

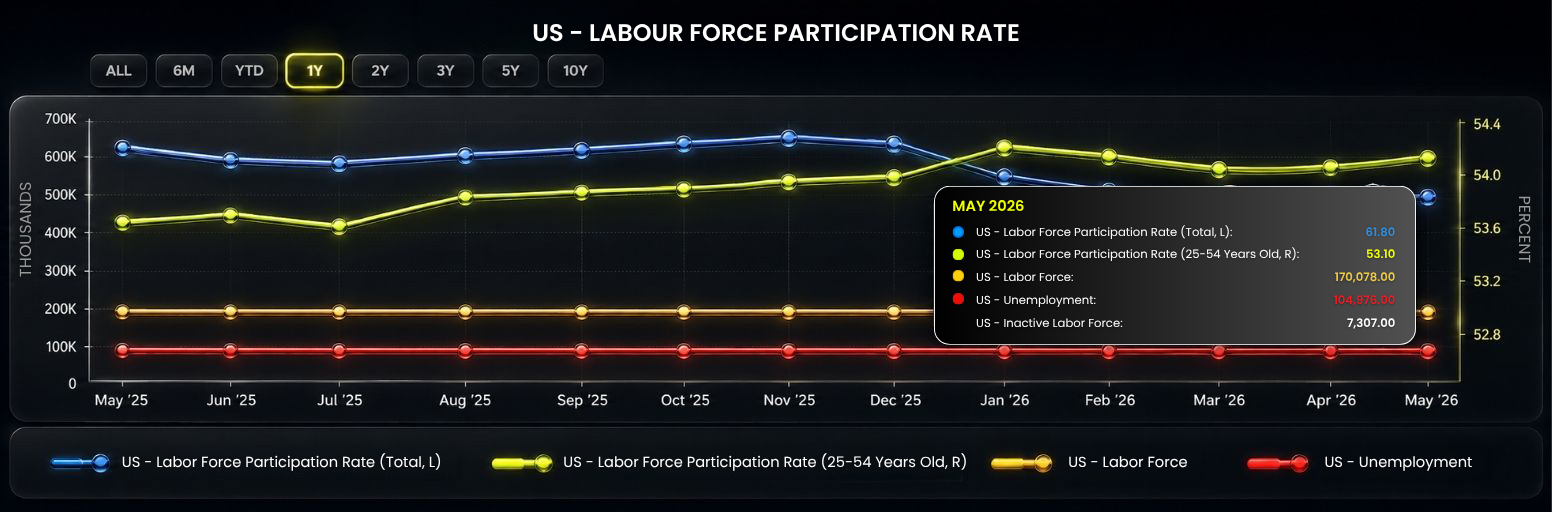

In May, the labor force participation rate stood at 61.8%, while the unemployment rate remained at 4.3%. Both figures were almost unchanged from April, suggesting that the labor market did not experience a major shift.

The current US labor force participation rate remains near one of its lowest levels in 40 years.

For the core 25-to-54 age group, labor force participation rose to 83.9%. Meanwhile, participation among people aged 55 and older remained stable.

However, the breakdown is not entirely positive.

Permanent layoffs rose significantly from the previous month, while temporary layoffs declined. This could suggest that companies are using part-time or short-term hiring to handle one-off demand related to the World Cup.

Once the World Cup effect fades, it remains uncertain whether employment can stay this strong.

The Labor Market Is Balanced, Not Overheating

Will upcoming non-farm payrolls reports continue to beat expectations by a wide margin?

Excluding the World Cup effect, that may be unlikely.

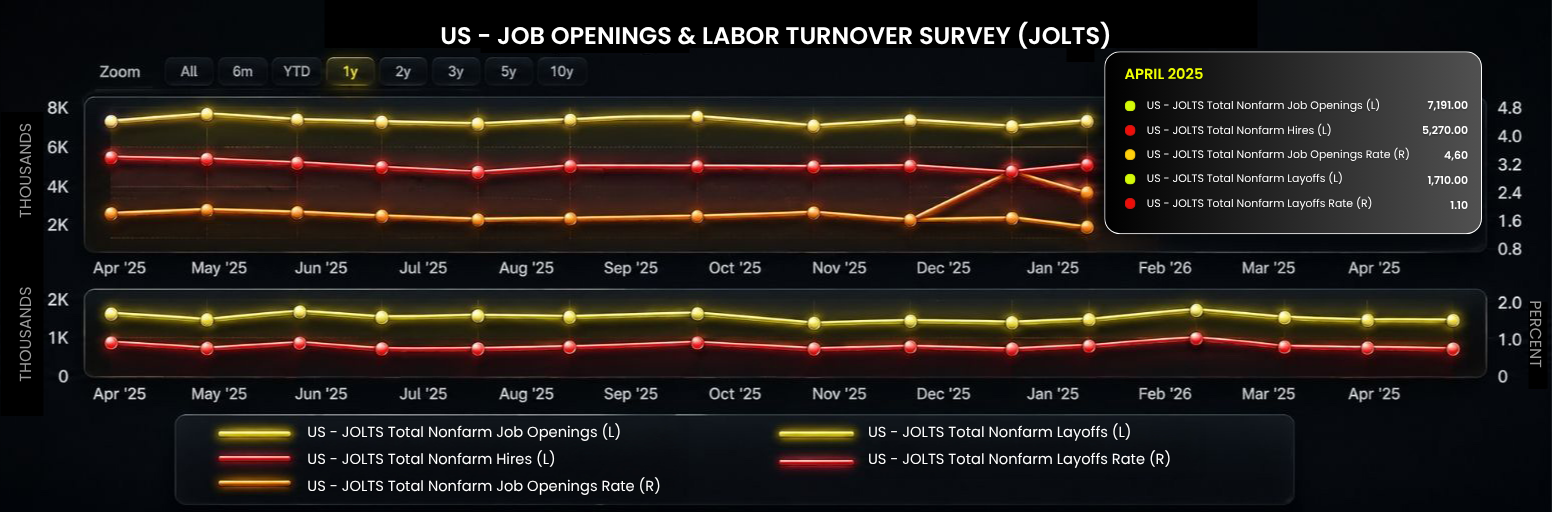

The JOLTS report showed that job openings reached 7.618 million in April, with the job openings rate at 4.6%, one of the highest levels in the past two years.

A rising job openings rate means more companies are trying to fill positions. But the US labor gap is also narrowing, suggesting the economy is close to full employment.

That points to a labor market that is broadly balanced between supply and demand.

This matters for the Fed.

A balanced labor market is not the same as an overheating labor market. It may not be enough to justify another rate hike, especially if other parts of the economy are already under pressure.

Inflation, Wages and Consumer Confidence Still Matter

Inflation remains one of the most important factors for the Fed.

The US-Iran conflict has affected the global inflation outlook, especially through oil prices. Crude oil has remained volatile, moving between USD 80 and USD 100.

However, recent crude market performance suggests that much of the risk may already be priced in. Inflation has not spiraled out of control beyond oil and other core commodities.

This suggests that even if Middle East tensions escalate, the upside for oil prices may be limited.

There are two reasons for this.

First, the market has become less sensitive to repeated geopolitical headlines. Second, higher oil prices can suppress demand. If fuel becomes too expensive, consumers may drive less and businesses may reduce energy consumption.

That limits the momentum for oil prices to rise sharply from current levels.

In our previous article, “April 2026 US Nonfarm Payrolls Beat Forecasts as Labor Market Weakens” we highlighted that hourly wages rose 3.6% year over year, missing expectations.

With oil prices still elevated, income growth is not keeping up with price pressures. That means consumers are losing purchasing power.

The weakness is even clearer across income groups. The lowest-income group is seeing the slowest hourly wage growth, while the middle class has the strongest wage growth, although its year-over-year growth rate is also falling.

Under these conditions, overall consumer spending power remains weak.

This pressure has pushed the University of Michigan Consumer Sentiment Index down to a 10-year low of 44.8.

That is important because rate hikes would add more pressure to an already fragile consumer environment. With consumer confidence deteriorating, the Fed may prefer to stay cautious.

Citi Still Expects Rate Cuts This Year

Based on observations, if the prices remain high, rate hikes are still possible.

However, the market may be overestimating the probability of a rate hike this year. The more likely scenario may be that the Fed holds rates steady through 2026, with any potential hike pushed into 2027.

But one major investment bank has made an even bolder call.

Citi believes the Fed may still cut rates this year.

Andrew Hollenhorst, Citi’s chief US economist, believes the US labor market could weaken over the next three months. Citi predicts that the Fed may cut rates by 25 basis points in September, October and December to support weakening employment.

The logic behind Citi’s rate-cut view is similar to D Prime’s observations.

The headline employment data looks strong, but the underlying details are less impressive. The current jobs boom may be temporary, partly supported by World Cup-related hiring and short-term labor demand.

That said, Citi’s forecast is much bolder than the market consensus.

It is also worth noting that Citi made a strong call last year. When many investors expected the Fed to keep rates steady, Citi accurately predicted three Fed rate cuts.

Politics may also play a role.

Trump remains a major pressure point for the Fed. In a Sunday interview on NBC’s Meet the Press, Trump said, “We built the country by doing great things and having interest rates low. When they raise rates, they are trying to kill success.”

If Fed Chair Warsh raises rates soon after taking office, political pressure could intensify quickly.

So, Will the Fed Hike, Cut or Hold?

The May 2026 non-farm payrolls report looked strong on the surface.

But beneath the headline number, the picture is more complicated.

A large share of job gains came from hospitality and government hiring, which may be linked to World Cup-related demand. Labor force participation remains low. Permanent layoffs have risen. Wage growth is not strong enough to offset inflation pressure. Consumer confidence is already weak.

That means the Fed may not be facing an overheating economy.

It may be facing a temporary jobs boost, sticky inflation and weakening consumers at the same time.

For traders, the key takeaway is simple: the market may be pricing in too much Fed tightening risk too quickly.

Based on current observations, it appears that the Fed is more likely to hold rates steady in 2026, unless inflation accelerates sharply again. Rate hikes remain possible, but the current probability may be overstated.

So what will the Fed do this year?

Raise rates, cut rates or hold steady?

For now, the answer may depend less on the headline jobs number and more on what happens after the World Cup hiring boom fades.

By D Prime Analysis Team

Macro and market strategy research by D Prime’s in-house analysis team.

Disclaimer

The information contained herein is provided for general informational and educational purposes only and does not constitute investment advice, financial advice, trading advice or any other form of professional advice, a recommendation, or an offer or solicitation to buy or sell any financial instruments or engage in any trading strategy.

Trading in leveraged products such as contracts for difference (CFDs) involves a significant risk of loss and may not be suitable for all investors. Past performance is not indicative of future results. Any references to market trends, asset performance, price levels, or forward-looking statements reflect opinions or general market commentary as at the date of publication and are subject to change without notice.

This article does not take into account any individual investor’s objectives, financial situation, or risk tolerance. Readers should conduct their own independent research and seek professional advice before making any investment or trading decisions. D Prime and its affiliates make no representations or warranties about the accuracy or completeness or reliability of this information and disclaim any and all liability for any direct, indirect, incidental, consequential, or other losses or damages arising out of or in connection with the use of or reliance on any information contained herein. The above information should not be used or considered as the basis for any trading decisions or as an invitation to engage in any transaction. Do not rely on this article to replace your independent judgment.

“D Prime” is a brand name of D Prime Vanuatu Limited, a company incorporated and regulated by the Vanuatu Financial Services Commission (Company Number: 700238). The availability of products and services may vary depending on jurisdiction and applicable regulatory requirements.