WORLDWIDE: HEADLINES

Japan Logs Biggest Current Account Deficit Since 2014 As Oil Import Costs Surge

Japan recorded its largest current account deficit since the start of 2014 in January as a jump in oil import costs offset gains in investment income, with continuing uncertainty due to the Ukraine crisis and COVID-19 pandemic.

The current account data highlighted the dependence of Japan’s resource-deficient economy on imports of commodities and raw materials, which caused trade deficit to widen.

Japan, the world’s third-largest economy, posted a current account deficit of 1.1887 trillion yen ($10.31 billion) in January, the data showed, versus economists’ median estimate of a 880 billion yen deficit in a Reuters poll.

It was the second straight month of deficit and marked the second largest deficit under comparable data going back to 1985.

Surging fuel costs drove up the value of imports by 39.9% in January from a year earlier, outpacing a 15.2% rise in exports.

In addition, Japan’s trade deficit with China widened in January. China-bound exports slowed before the Lunar New Year break while imports from the country surged due to stocking demand before the holiday period.

“Given such a temporary factor and a hefty investment income surplus, I don’t think Japan’s balance of payment will swing to deficit as a trend anytime soon,” said Takashi Miwa, chief economist at Nomura Securities.

Japan earns steady and hefty return from its past investment in securities and direct investment overseas, which have replaced trade as the main driver of its current account surplus in recent years.

While a weak yen also helped inflate the cost of imports, its boost to export volumes was not as great as it once was due to an ongoing shift of exporters’ production abroad, analysts say.

Full coverage: REUTERS

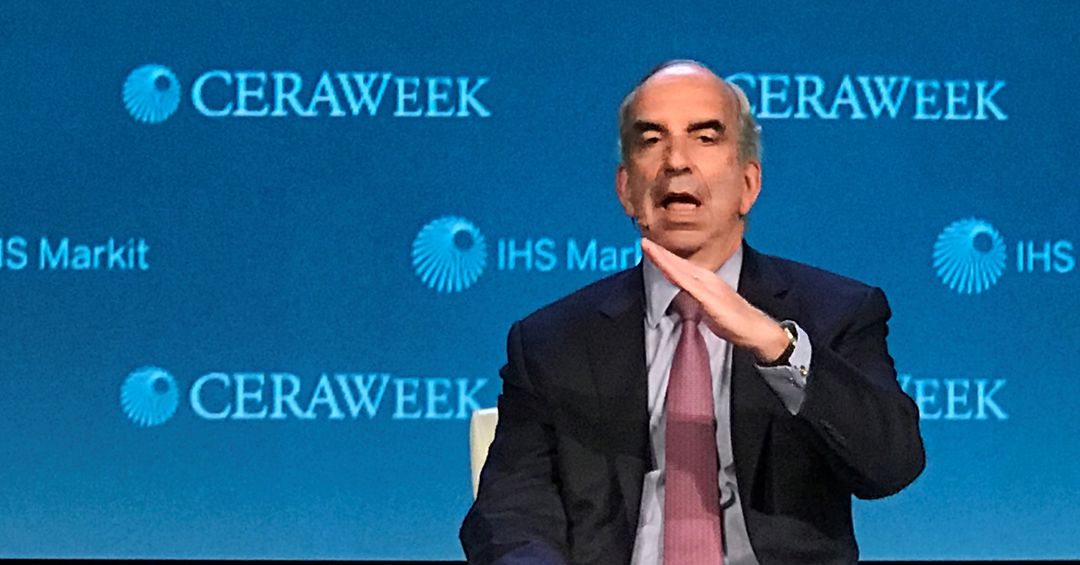

OPEC Meet With U.S. Shale Executives At U.S. Energy Conference As Oil Prices Skyrocket

Officials from the Organization of the Petroleum Exporting Countries on Monday met with executives of several top U.S. shale oil companies at a top U.S. energy conference as energy prices soared over supply concerns.

Oil hit a 14-year high of $139 a barrel earlier on Monday as worries grew over supply shortages as buyers shunned cargoes from No. 2 oil exporter Russia. Earlier, OPEC Secretary General Mohammad Barkindo said at the CERAWeek energy conference that OPEC could not offset a ban on Russian oil exports.

EQT Corp. Chief Executive Toby Rice and Hess Corp CEO John Hess attended the dinner held at The Grove restaurant adjacent to the CERAWeek conference site, according to a Reuters witness. It was at least the fourth time that U.S. shale oil producers and OPEC officials broke bread to discuss energy concerns.

A spokesperson for Barkindo did not reply to a request for comment. A Hess spokesperson who accompanied its CEO declined to comment.

Full coverage: REUTERS

WORLDWIDE: FINANCE/BUSINESS

Oil Seesaws, Asia Shares Dip As Ukraine Talks Make Little Progress

Oil prices gyrated and Asian shares fell on Tuesday as Ukraine peace talks made little headway and the prospect of a ban on oil imports from Russia triggered investor fears over inflation and slowing economic growth.

President Joe Biden’s administration is willing to move ahead with a U.S. ban on Russian oil imports even if European allies do not, Reuters reported on Monday, citing two people familiar with the matter.

Oil prices have already hit 14-year highs and Russia warned that prices could surge to $300 a barrel and it might close the main gas pipeline to Germany if the West halts oil imports over the invasion of Ukraine.

MSCI’s broadest index of Asia-Pacific shares outside Japan (.MIAPJ0000PUS) lost 0.4% in early trade, tracking a bruising Wall Street session. Japan’s Nikkei (.N225) sank 0.3% while Australian shares (.AXJO) were down 0.24% amid a sea of red across Asian markets.

Chinese blue chips (.CSI300) shed 0.15% while Hong Kong’s Hang Seng index rose 0.39% .

International oil benchmark Brent crude, which briefly hit more than $139 a barrel in the previous session, jumped around in morning trade and was up about 0.8% at $124.20.

U.S. crude was up about 0.4% at $119.86 a barrel, while prices of many other commodities, including nickel, rose as industrial buyers and traders scramble as the Russian-Ukraine conflict shows no sign of cooling.

“Global risk sentiment started the week deeply negative, before improving as European leaders indicated they would resist sanctions on Russian energy exports, preferring instead a determined strategy to reduce dependency on Russian imports,” ANZ analysts said in a note.

“Markets are volatile, however, and highly sensitive to shifts in tone. The progressive rise in breakeven inflation rates is evidence of mounting inflation concerns as commodity prices remain firmly underpinned.”

Full coverage: REUTERS

Euro Mired While Ukraine War Weighs On Growth

The euro was pinned near a 22-month low on Tuesday as war in Ukraine has darkened Europe’s economic outlook, while commodity currencies took a breather in their weeks-long rally.

The euro was doing its best to bounce after six straight sessions of selling, but at $1.0855, it was not terribly far from Monday’s trough of $1.0806.

The common currency is down 4% on the dollar since Russia launched what it calls a “special military operation” in Ukraine where fighting is showing no signs of abating. It flirted with parity on the Swiss franc on Monday for the first time in seven years.

Russia-Ukraine Peace talks have made scant progress and though Germany’s opposition to a ban on Russian energy imports knocked oil futures from Monday’s 14-year peak, analysts expect the supply shock to hurt European growth.

“Markets could continue to price the risk of a disruption to Russian energy exports and downgrade the European growth outlook,” said Commonwealth Bank of Australia strategist Carol Kong.

“As such, we expect the euro to remain under pressure. There is a reasonable chance euro/dollar tests the pandemic low of $1.0688 this month.”

The European Central Bank meets on Thursday with the spectre of stagflation prompting economists to figure that policymakers might delay rate hikes until late in the year.

Besides commodities’ parabolic rally the conflict and subsequent sanctions have crushed Russian assets, with the rouble sliding to a record low of 160 to the dollar in erratic offshore trade on Monday.

Elsewhere the U.S. dollar was firm amid nerves the war and its economic consequences could spread.

Surging oil import costs already pushed Japan to its largest currency account deficit since 2014, knocking some of the lustre from yen as a safe-haven.

Full coverage: REUTERS

Oil See-saws Near 14-yr Highs As U.S. Weighs Russia Oil Embargo

Oil prices see-sawed near 14-year highs on Tuesday as the United States considered acting alone to ban Russian oil imports rather than teaming up with allies in Europe, easing concerns of a wider disruption to crude supplies.

Brent crude futures were up $1.06, or 0.9%, at $124.27 a barrel at 0223 GMT, after trading as high as $125.19 then dipping to $121.31.

U.S. West Texas Intermediate (WTI) crude futures were up 36 cents, or 0.3%, at $119.72 a barrel after also trading in a roughly $4 range.

The erratic moves came following a sharp run-up on Monday to near 14-year highs when the Biden Administration said it was talking to Britain, France and Germany about a ban on Russian oil.

“The price move up has been far too aggressive in too short a time. The charts are telling us the oil price needs to do some digesting before it can move substantially higher,” said Michael McCarthy, chief strategy officer at Tiger Brokers Australia.

Keeping a lid on price gains, late on Monday officials said the United States was willing to move ahead with a ban alone, and Germany, the biggest buyer of Russian crude, rejected plans for an energy embargo.

A senior U.S. official, speaking on condition of anonymity, told Reuters no final decision had been made but “it is likely (to be) just the U.S. if it happens.”

Russia exports around 7 million barrels per day of crude and oil products.

“Markets though have already priced in a significant disruption to Russian oil exports already,” Commonwealth Bank commodities analyst Vivek Dhar said in a note, pointing to how sanctions on Russian banks have already hit trade finance.

If all of Russia’s oil exports were blocked from global markets, analysts have said prices could rocket to $200 a barrel, while Russia’s deputy prime minister said oil could soar to more than $300.

Full coverage: REUTERS